As we approach the anticipated sunset of the Tax Cuts and Jobs Act (TCJA) in 2026, you may be wondering whether now is the time to make adjustments to your tax, estate, or investment strategy. Although planning ahead is tempting, tax laws often shift based on government policies. Given the original TCJA was enacted during Trump’s first presidency, it’s highly likely that some provisions will be extended or replaced with an entirely new tax framework. Rather than making hasty decisions based on the concern for sunsetting, it’s best to stay informed and remain flexible until we have more clarity on what’s next.

In order to understand whether changes to the TCJA would affect you, let’s take a look at five of the most influential tax changes that are set to sunset in 2026.

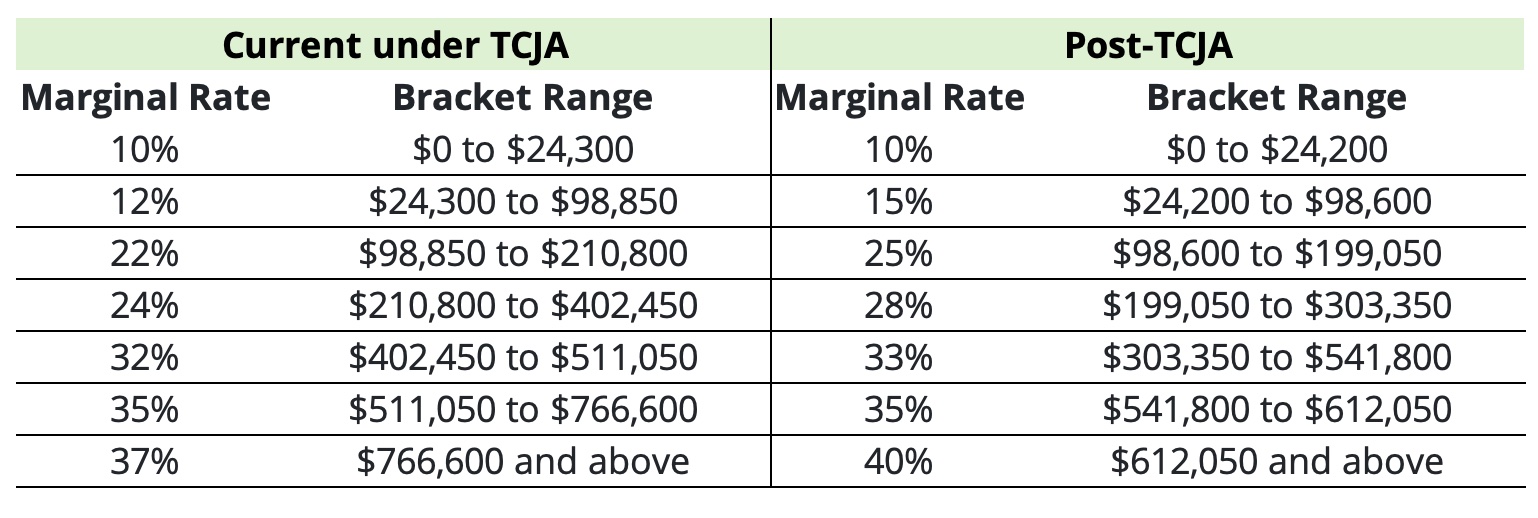

Tax Brackets

Perhaps the most relevant change for any taxpayer, the TCJA changed five out of the seven tax rates and bracket ranges:¹

Above illustrates a comparison for a married filing jointly couple using assumptions from our Holistiplan tax planning software. The left shows how current rates and brackets could look in 2026 if TCJA was extended. The right illustrates an inflation-adjusted reversion back to brackets and rates as last seen in 2017.

Note: Marginal tax rates refer to the percentage of tax you pay on each additional dollar of income, based on the tax bracket you fall into. The U.S. tax system is progressive, meaning different portions of your income are taxed at different rates. Therefore your effective (or average) tax rate is typically different than your marginal tax rate.

Marginal income tax brackets apply to ordinary income, which includes:

- Wages & Salaries – Employment income from a job (W-2 income).

- Self-Employment & Business Income – Profits from sole proprietorships, partnerships, and LLCs (subject to self-employment tax).

- Bonuses & Commissions – Extra compensation from employment.

- Freelance & Side Gig Earnings – Income from contract work (1099 income).

- Interest Income – Interest from bank accounts, CDs, and taxable bonds (not tax-exempt municipal bonds).

- Short-Term Capital Gains – Profits from selling investments held for one year or less.

- Rental & Passive Income – Net income from rental properties (after expenses).

- Retirement Account Withdrawals – Distributions from traditional IRAs, 401(k)s, and other pre-tax accounts (except Roth accounts, which are tax-free if qualified).

- Unemployment Benefits – Taxable income received from unemployment compensation.

- Alimony (if divorce finalized before 2019) – Spousal support payments (not applicable for divorces after 2018 due to TCJA changes).

Marginal tax brackets do not apply to:

- Long-term capital gains (for assets held over a year)

- Qualified dividends (which follow long-term capital gains rates)

- Roth IRA withdrawals (if qualified)

- Life insurance proceeds

- Tax-exempt municipal bond interest

Personal Exemption Phaseout (PEP)

The TCJA suspended the personal exemption, meaning it’s set to return in 2026 (unless further legislative action takes place). It’s important to note that the personal exemption can still be claimed on your tax return, though the rate is set to $0. Claiming the exemption—even though it’s not worth a dollar amount—could potentially make you eligible for other tax benefits.²

Prior to the TCJA, the personal exemption was a fixed amount individuals could deduct from their taxable income, as long as they weren’t claimed as dependents on someone else’s return. The personal exemption did include phaseout limits, meaning high earners who exceeded the annual income limit would not be eligible for the exemption.

For reference, the personal exemption in 2017 (the last year it was available) was $4,050 per person with a full phaseout for those with adjusted gross incomes above $384,000 or $436,300 for joint filers.³

Deductions & Credits

The standard deduction got a boost as part of the TCJA, which made the percentage of taxpayers who chose to itemize drop significantly. In 2020, for example, only 10% of taxpayers chose to itemize their deductions.⁴

The standard deduction got a boost as part of the TCJA, which made the percentage of taxpayers who chose to itemize drop significantly. In 2020, for example, only 10% of taxpayers chose to itemize their deductions.⁴

Considering the standard nearly doubled when the TCJA was enacted, it’s possible taxpayers could see the standard deduction cut in half by 2026 if the provision sunsets. In 2025, the standard deduction will be $15,000 for individual filers and $30,000 for joint filers.⁵

At the same time, the TCJA reduced some common itemized deductions (further incentivizing taxpayers to opt for the standard route).

These include:⁶

- State and local taxes (SALT): The TCJA currently caps the SALT deduction at $10,000. Reverting back to pre-TCJA guidelines could make it unlimited.

- Mortgage interest: Taxpayers can currently deduct mortgage interest on loans up to $750,000. Pre-TCJA, the loan limit was larger (when adjusted for inflation).

- Charitable donations: Under TCJA rules, taxpayers can donate and deduct up to 60% of their AGI. In pre-TCJA rules, the AGI percentage drops to 50%.

- Medical expenses: The TCJA allows taxpayers to deduct unreimbursed medical expenses that exceed 7.5% of their AGI. Prior to the TCJA, the expenses needed to exceed 10% of the taxpayer’s AGI.

The TCJA also eliminated a few previously available deductions including:⁶

- Financial advisory fees

- Tax preparation fees

- Unreimbursed employee expenses

- Theft and personal casualty losses (unless the loss occurs in a federally declared disaster area)

Child Tax Credit

The TCJA increased the child tax credit to $2,000, with a maximum refundable portion up to $1,700. If the child tax credit reverts back to pre-TCJA rulings, it will likely drop to $1,000—though the full amount will be refundable for eligible taxpayers.⁷

Higher Taxes on Small Businesses & Pass-Through Entities

One of the most significant benefits for small business owners under TCJA has been the 20% Qualified Business Income (QBI) deduction, which allows pass-through entities—such as sole proprietorships, S corporations, and partnerships—to deduct up to 20% of their business income before calculating taxes. This deduction effectively reduces the tax burden for millions of small business owners. If Congress does not extend or revamp this provision, pass-through businesses will face higher taxable income, potentially pushing them into higher tax brackets and increasing their overall tax liability.

Additionally, without the QBI deduction, certain professional service businesses—such as law firms and consulting practices—that already face phase-outs at higher income levels will see an even greater tax impact. With corporate tax rates remaining at 21% (unless changed by future legislation), some pass-through entities may reconsider their business structure, potentially opting to convert to C corporations if the tax advantages align better with their long-term strategy. However, with C corporations subject to double taxation (corporate tax + dividend tax), this decision requires careful evaluation. Business owners should work closely with tax professionals as more information becomes available on how QBI will be handled come 2026.

Estate and Gift Tax Exemption

The IRS allows taxpayers to transfer a certain amount of wealth to loved ones before incurring any tax liability, including gifting during your lifetime or passing along an inheritance after death. This lifetime exemption limit doubled in 2017 as part of the TCJA and currently sits at $13,990,000 per individual, or $27,980,000 per couple.⁵ Should the rulings revert back in 2026, we could see the estate tax exemption limit drop back to $5,000,000 indexed for inflation. Once inflation is factored in, this would land around $7,000,000 per individual.

What Can Taxpayers Expect in 2025 and Beyond?

With President Trump back in office this year, it’s likely we’ll gain clarity on which provisions will be extended or revamped. Until any legislative action is taken, however, it may be wise to simply discuss potential strategies that could be relevant given various outcomes in the 2026 tax year.

Depending on your goals, you might want to take advantage of the current tax rates and exemption limits before they potentially hike back up (or drop-down, as the case may be) to pre-TCJA levels.

Feel free to reach out to our team to talk through these provisions, and discuss how impending tax legislation may impact your tax planning strategies for 2026 and beyond.

Sources:

1 How 2026 Tax Brackets Would Change if the TCJA Expires

3 Tax Changes You Need to Know for 2017

4 What are itemized deductions and who claims them?

5 IRS releases tax inflation adjustments for tax year 2025

6 How did the TCJA change the standard deduction and itemized deductions?

7 Reference Table: Expiring Provisions in the “Tax Cuts and Jobs Act” (TCJA, P.L. 115-97)