When you have a complex tax situation, there’s likely so much on your mind heading into tax season.

Here are a few tips to keep in mind before filing your 2021 tax return.

1. Prep For An AMT Tax Bill

Alternative Minimum Tax (or AMT) is a parallel tax filing system designed to ensure that high-earners pay enough taxes. There are two rates—26% and 28%.

You may be subject to AMT if you exercised a lot of ISOs (Incentive Stock Options), have high state and local taxes, have a high salary, or live in an area with a high cost of living. With ISOs, the spread (the difference between your purchase price and the stock’s fair market value) isn’t immediately taxable, but it does count toward your AMT calculation.

Unfortunately, you can’t take a SALT deduction with AMT. The SALT deduction allows taxpayers to deduct state and local taxes paid from their federally taxable income, protecting individuals and families from double taxation and local governments’ decision-making authority.

Be sure you know what your tax bill is and that you have the immediate funds to pay it. Perhaps you’ll pull from a cash reserve or liquidate investments to cover the tax bill. In either case, the more prepared, the better.

2. Take Stock Of Your Vested Equity (And What’s On The Horizon)

Equity compensation is a dynamic area that requires a unique strategy to get right.

Take a look at what equity has vested over the last year. Ask yourself the following questions:

- Should you exercise any options before tax time?

- What’s your strategy for exercising throughout the year?

- Could there be an equity event that catapults you into a much higher than anticipated tax bracket?

It can be beneficial to exercise at the beginning of the year if possible. That way, you have time to see how the market performs, assess your status with the company, prep for any tax bills, etc.

3. Make A Tax-Friendly Charitable Giving Plan

Charitable giving is an integral part of many people’s lives, personally and financially. While the primary effort of giving is supporting causes you care about, high earners may also be able to take advantage of tax benefits for their generosity.

If itemizing your deductions, you can give to charity in several ways such as,

- Give a check, cash, stock, etc., directly to a charitable organization or non-profit.

- Open a Donor Advised Fund (DAF) and contribute cash, stock, etc.

- Establish and fund your own Charitable Giving Foundation.

- Make Qualified Charitable Donations (QCDs) directly from your IRA.

- Bunch charitable donations.

When donating stock, it is most advantageous to give appreciated securities, thus capitalizing on the tax deduction and avoiding capital gains tax.

A popular giving strategy of late is bunching charitable donations or concentrating on giving more substantial charitable gifts every couple of years. Since the Tax Cuts and Jobs Act increased the standard deduction by such a high margin, many families couldn’t take advantage of itemizing as often.

But by bunching your giving, you can take the standard deduction in some years and itemize in others. One way to do this is to contribute a considerable amount to a donor-advised fund (DAF) in one year and then, in subsequent years, grant the funds from your DAF to your charities of choice. Bunching can be ideal in years when you have a higher reportable income.

If you’re not itemizing this year, you can still reap some tax rewards for your gifts. The IRS extended the enhanced charitable giving provision in the CARES Act, enabling people to deduct up to $300 ($600 married filing jointly) in cash gifts to qualified charities. Keep in mind that while you can give via cash or a check, physical goods and donations don’t count.

4. Read IRS Letter 6419

Did you receive advanced payments for the expanded child tax credit?

If so, it will be a good idea to take a look at IRS Letter 6419 because it details how much you received against what you’re actually eligible to claim based on your 2021 tax return.

The IRS released a notice saying that many of the forms were wrong, and it is important to tally up how much money you received throughout the specified period. This situation was even true for one of our Wingate advisors!

If your monthly checks were too high, you might end up owing the IRS. Be sure to keep this form and give it to your CPA or tax professional so they can help you sort everything out.

5. Make Estimated Tax Payments As You Move Into Retirement

There’s so much to think about and plan for when you transition into retirement, especially where taxes are concerned.

For example, we often see people with high wages (that previously had automatic withholdings) retire and start drawing from retirement accounts, pensions, Social Security, etc. In addition to these income sources, they also have reportable investment earnings.

Once you’re in retirement and utilizing all of these channels to create your income, it is your responsibility to ensure that your withholdings are where they need to be. In most cases, you’ll need to make estimated tax payments (ETPs).

Therefore, it is critical to make ETPs throughout the year and elect the appropriate amount of withholdings from retirement income sources, like an IRA, when possible.

Why is this so important?

If you don’t withhold and pay enough taxes throughout the year, you could be at risk for an underpayment penalty.

The IRS will not charge you an underpayment penalty if:

- You pay at least 90% of the tax that you owe for the current year, or

- You pay 100% of the tax that you owed for the previous tax year, or

- You owe less than $1,000 in tax after subtracting withholdings and credits

There are some slight alterations in the rules for high-income taxpayers. If the adjusted gross income (AGI) on your previous year’s return is over $150,000, you must pay the lower of:

- 90% of the tax shown on the current year’s return, or

- 110% of the tax shown on the return for the previous year

Alongside the federal requirements, each state will have its own rules and regulations. Be sure to consider your state ETPs, in addition to your federal ETPs, as you plan for your tax liability throughout the year.

6. Be Aware Of Phaseouts, Taxes, and Surcharges As A Higher-Earner

In addition to keeping an eye on ordinary income and capital gains tax brackets, it is also worth considering the various phaseouts, taxes, and surcharges that could apply to you as a high-earner.

While this list is not all-encompassing, a few to be aware of include:

- Roth IRA contribution phaseouts

- Medicare IRMAA (Income Related-Monthly Adjustment Amount)

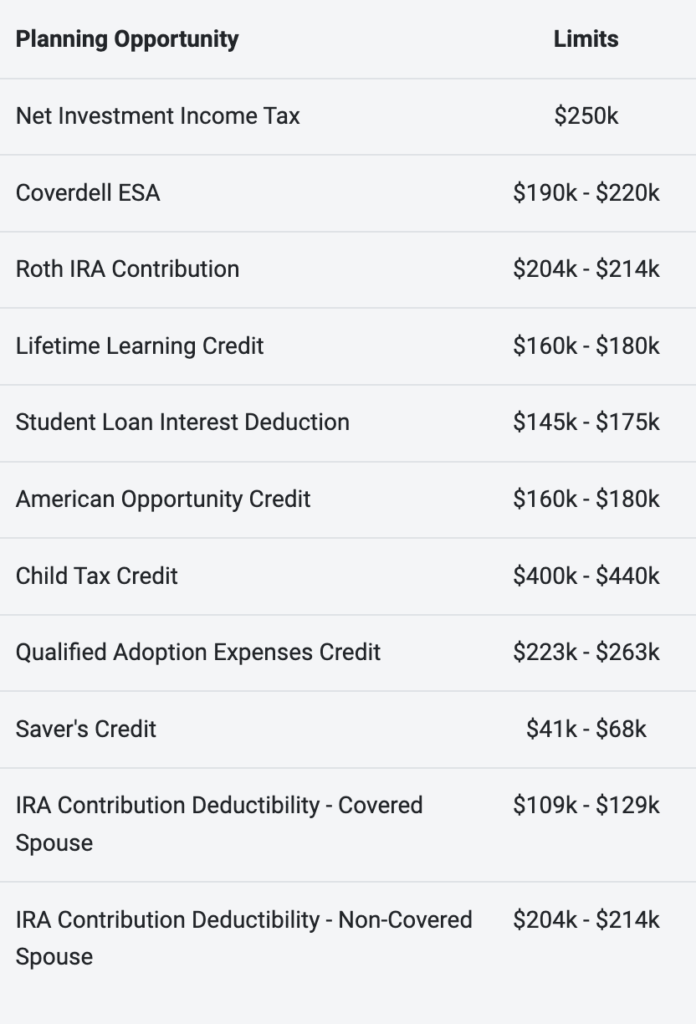

- 3.8% Net Investment Income Tax (NIIT)

The Net Investment Income Tax hits many high-earning couples as it’s threshold only increases by $50,000 instead of doubling when compared to a single filer. See below thresholds for a married filing jointly couple:

Our team can help you manage your tax bracket and offer sage advice about strategies for realizing gains, lowering your adjusted gross income, and more.

7. Work With A Financial Team You Trust

Proactive tax planning is critical for executives with various income sources like equity compensation. We can help you build a strategy that keeps the bigger picture in mind. It is also imperative to work with a CPA, EA, or other tax professional to help execute your strategy.

Our goal is to help clients see their complete picture and guide them in taking steps that optimize their long-term goals.

Wingate Wealth Advisors can analyze your case, make strategic recommendations, and help you execute the most effective strategies for you. Contact us today.