The government is making a wide range of adjustments across the board for the coming year. Changes impactMedicare premiums, Social Security COLA, tax brackets, and retirement plan contribution limits. The changes could mean higher income and tax savings for some next year.

Medicare Part B Premiums have decreased. The base monthly premium for Medicare Part B enrollees will now be $164.90 for 2023, a decrease of $5.20 from 2022. The annual deductible for all Medicare Part B beneficiaries is $226 in 2023, a decrease of $7.00.

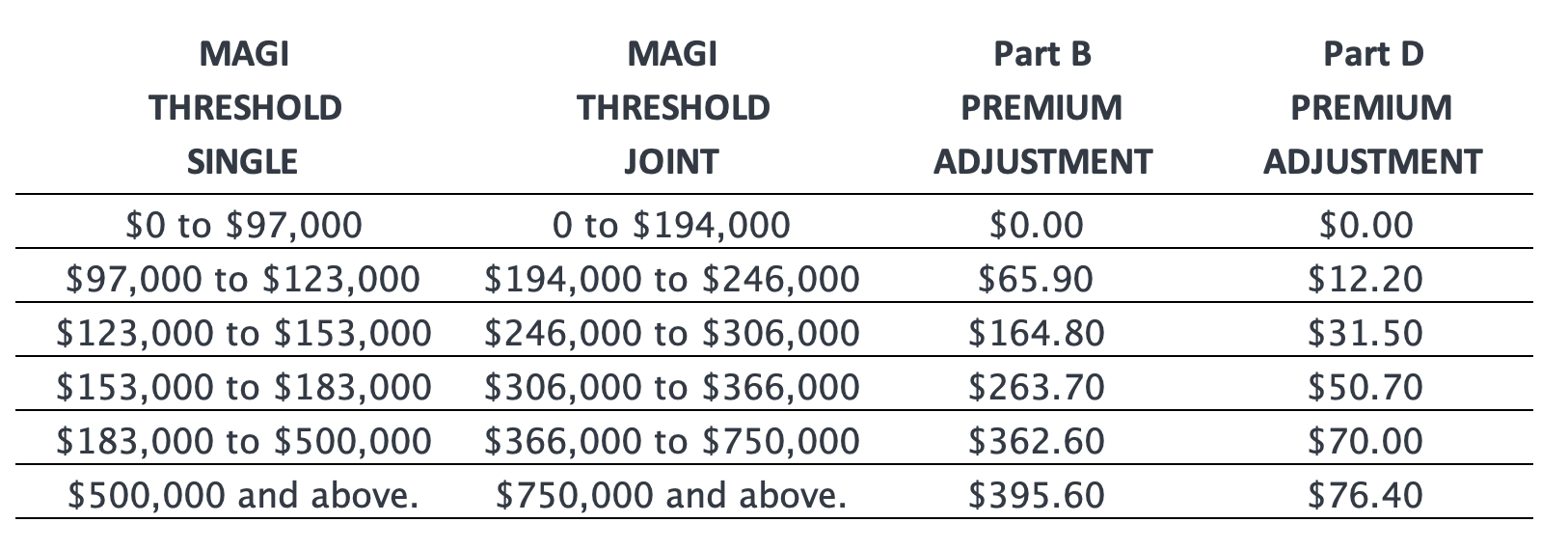

Medicare premiums are adjusted based on income, meaning higher income enrollees pay $164.90 for Part B and about $31.50 for Part D plus the adjustment. IRMAA Brackets and adjustments for 2023 are as follows:

You may also notice a new premium table that may or may not apply to you. Beginning in 2023, certain Medicare enrollees who are 36 months post kidney transplant, and therefore are no longer eligible for full Medicare coverage, can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. For more information on this specifically, read on here.

The Medicare Part A has no premium to the extent you or your spouse qualify by having 40-quarters (10-years) of eligible work history. That said, there are deductibles and co-insurance amounts that increased from 2022.

In terms of coverage, a big win in 2023 is related to prescriptions. The cost of insulin will be capped at $35 for a 30-day supply, and most vaccines will be free. This includes the popular shingles vaccine. More changes are slated for 2024 and 2025 related to capping out-of-pocket costs entirely and limiting premium increases. While mostly good news, the max Part D deductible edged up slightly and is now $505/year compared to $480 in 2022.

The favorable changes made via the Tax Cuts and Jobs Act are set to sunset after 2025. Until then we may not see any material changes apart from normal inflation adjustments to the brackets. See chart for updated brackets, no changes to the rates.

The standard deduction for single taxpayers in 2023 will rise by $900 to $13,850, and increase for married taxpayers filing joint returns by $1,800 to $27,700.

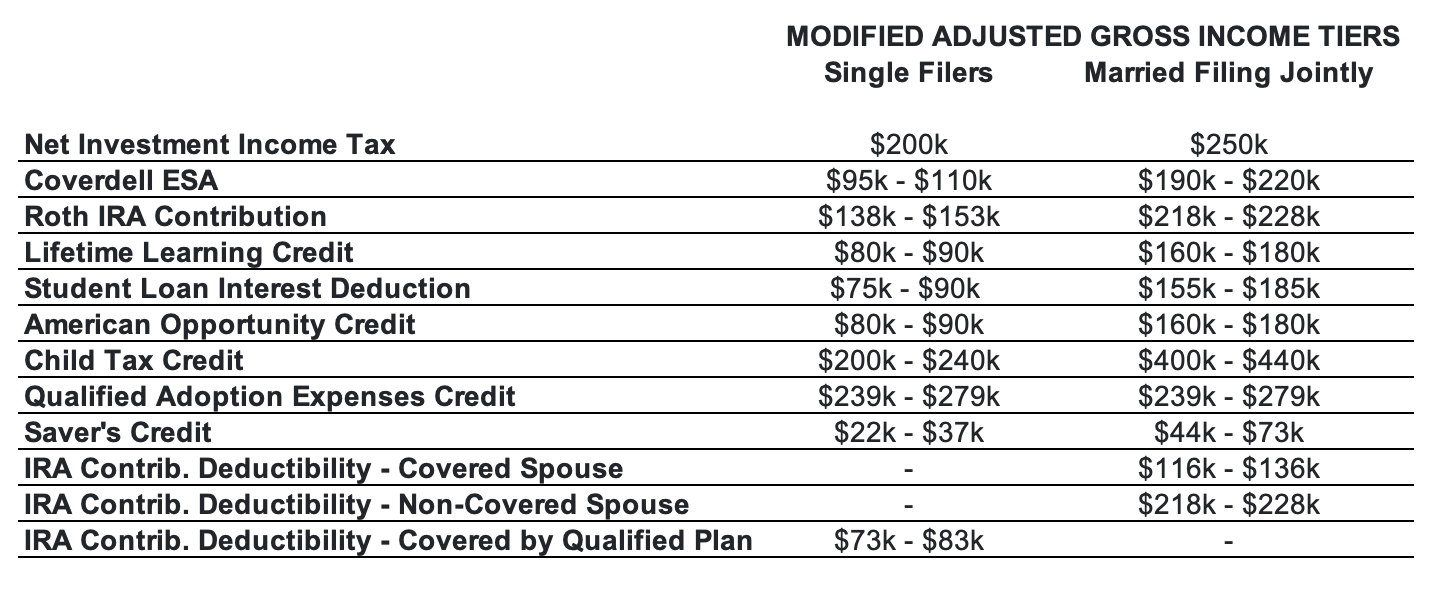

As it relates to the finer points of a tax return, ie – various deductions and credits, see the following chart. There has been no adjustment to the Net Investment Income Tax or the Child Tax Credit thresholds.

Click here for the full announcement related to income tax adjustments.

Click here for the full announcement related to income tax adjustments.

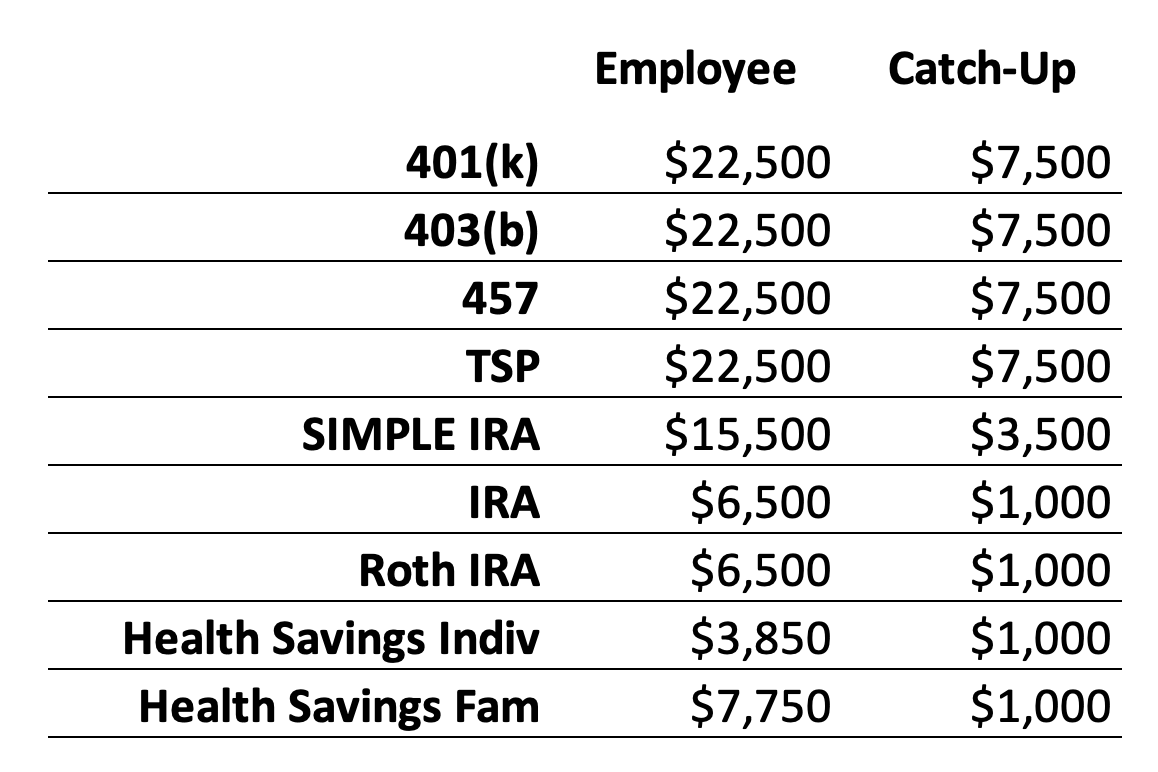

Updated employee benefit packages are starting to roll out, and you may be asked to make or confirm contribution elections toward retirement plans and health savings accounts. There are increases across the board in 2023 for how much can be contributed. See our chart for the most popular plans.

Updated employee benefit packages are starting to roll out, and you may be asked to make or confirm contribution elections toward retirement plans and health savings accounts. There are increases across the board in 2023 for how much can be contributed. See our chart for the most popular plans.

IRS Release on Increased Limits.